The Space Ecosystem Re-Entry: Post-IPO Correction Creates the Entry Point

Institutional Cross-Asset Market Intelligence

This report is part of our cross-asset “What Matters” publication, a new, differentiated product available via a separate subscription. To access the full analysis, please upgrade below or contact us at info@10xresearch.com with any questions.

Introduction / encouragement to read the PDFs:

The SpaceX IPO has landed. The first wave of the trade is behind us. What comes next is more interesting: a post-IPO correction that has reset entry points across the entire ecosystem, from the pure-play high-beta names to the Taiwanese suppliers the institutional indices have never heard of.

This report sets out exactly where we are looking to re-enter and why the multi-year thesis is intact. To get the full picture, we strongly encourage subscribers to read both attachments alongside this note. The 20-page chart book gives you the complete technical picture, every name in the index with 7-day and 30-day moving average signals, relative strength versus SpaceX, and Top Chart designations. The 19-page consolidated report, After Liftoff: The SpaceX IPO Has Landed — Now the Real Ecosystem Trade Begins — provides the full investment framework: the SpaceX valuation gap, the supply chain thesis, the regression analysis, and the company-by-company breakdown across all ten categories. Together they represent two to three months of primary research on the most important new investment theme of 2026. Start there.

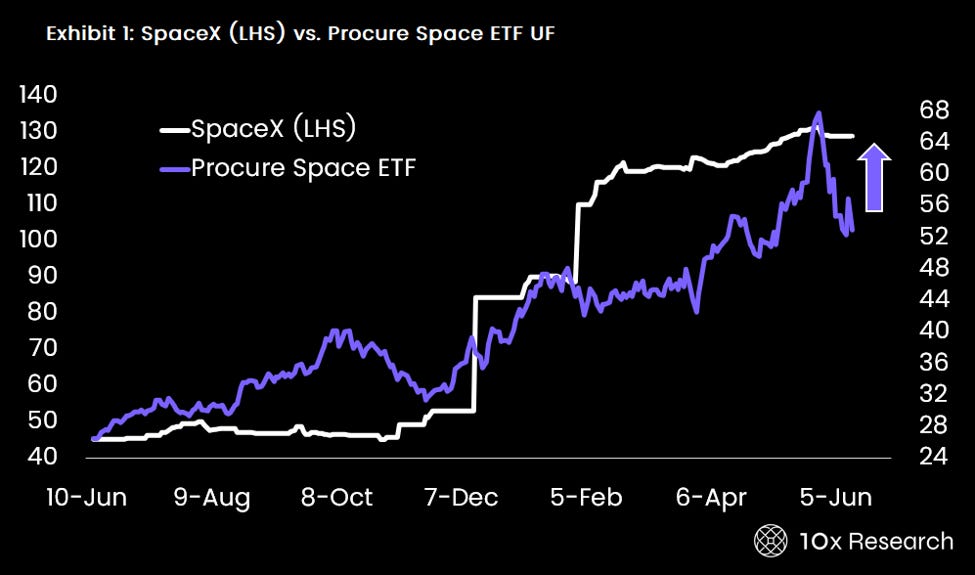

The Blue Origin explosion on May 28, 2026, triggered a sharp correction across space stocks that has extended through the SpaceX IPO, as investors rotated out of the higher-beta names and into SpaceX directly. That rotation is understandable, but ultimately misses the point. SpaceX itself has evolved into an aggressive AI and data infrastructure company. Starlink is as much a computing layer as it is a satellite network, whereas the smaller pure-plays and supply chain names are more purely exposed to the space economy itself. Over a multi-year horizon, we expect the broader ecosystem to outperform SpaceX as the IPO premium fades and the market begins to price in the supply chain opportunity more systematically.

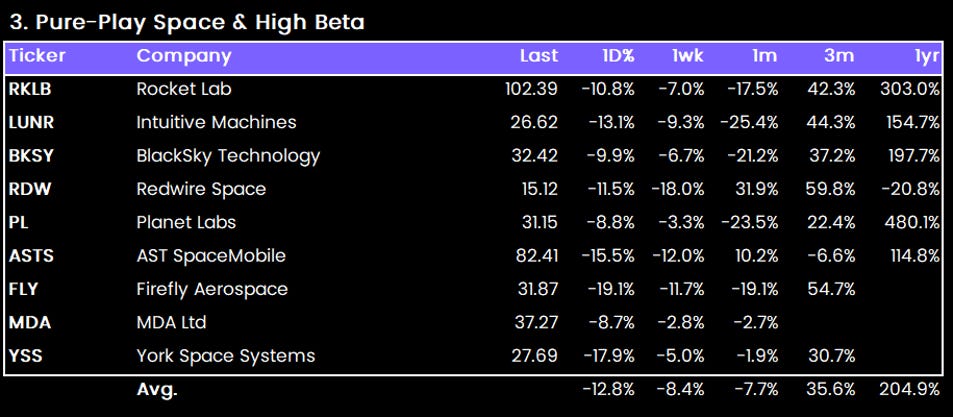

The pullback has created compelling re-entry levels across the index. On the pure-play side, we are watching the UFO ETF near $48, Rocket Lab in the low $90s, Intuitive Machines around $23, BlackSky Technology near $28, Redwire Space at $12, and Planet Labs around $26. These are levels where the risk/reward tilts back in favor of the bull case.

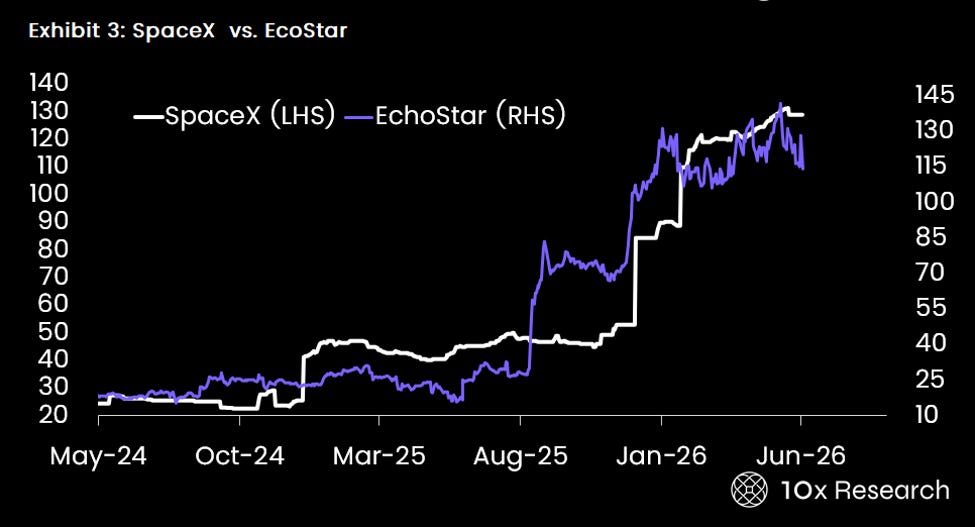

On the supplier side, the four Taiwanese names, Compeq, Universal Microwave, Tong Hsing, and WNC Corp, remain our highest conviction longer-term positions despite their small-cap liquidity constraints. These companies are structurally embedded in the Starlink production ramp and will compound quietly long after the IPO excitement has moved on. Filtronic near £300 and CPS Technologies around $6 round out the supplier watchlist as two of the most direct and highest-leverage SpaceX proxies available in listed markets.

Why We Like These Three Categories

Pure-Play Space & High Beta (RKLB, LUNR, BKSY, RDW, PL, ASTS, FLY, MDA, YSS)

This is the highest-conviction, highest-volatility bucket in the index, the names that move most directly with the SpaceX narrative and reprice most aggressively around catalysts. The category averaged +205% over the past year, reflecting the scale of the re-rating that has already occurred, as well as the magnitude of the correction opportunity now that the post-IPO pullback has reset entry points. These are not value stocks. They are optionality instruments on the commercialization of space, and they should be sized accordingly. The right approach is to treat this bucket as the high-beta core of a space allocation, own the names with the strongest relative strength signals (RKLB, ASTS, RDW currently flagged as Top Charts), keep position sizes disciplined given the drawdown potential, and use the 7-day and 30-day moving average framework (see attached PDF chart book) to time entries rather than buying into weakness indiscriminately. The average 3-month return of +35.6% with a 1-month pullback of -7.7% is a textbook consolidation setup within a larger uptrend.

SpaceX Suppliers — Taiwan, Korea & UK (FTC.L, WNC, Compeq, Universal Microwave, Tong Hsing, CPSH, Sphere Corp)

This is the most proprietary and least-crowded bucket in the index, names that most institutional investors have never modeled. These companies supply the RF components, ceramic substrates, PCBs, and thermal management hardware that go into every Starlink satellite and ground terminal SpaceX produces. Their revenues are not correlated to SpaceX’s stock price, they are correlated to SpaceX’s production volume, which is a fundamentally different and more durable driver. The 3-month average return of +46.3%, with a 1-year average of +229.5%, reflects what happens when a supply chain that has been quietly compounding is discovered by the market. The investment approach here is different from the pure-plays: these are not momentum trades to be timed around catalysts, they are structural positions to be built during pullbacks and held through the multi-year Starlink production ramp. The weekly volatility can be severe; CPSH was up +142% in a single week, so position sizing must account for liquidity and bid-ask spreads, particularly in the Taiwanese and Korean names. These are not names to chase after a 30% week; they are names to accumulate on red days when the broader space theme is under pressure.

Electronics & Semiconductors (MRCY, TTMI, MTSI)

This is the most defensible bucket in the index, companies with deep defense and government contract backlogs that provide revenue visibility independent of any single space program or IPO event. Mercury Systems, TTM Technologies, and MACOM are not pure space plays; they are defense electronics businesses that are deeply embedded in both the military satellite architecture and the commercial LEO supply chain. That dual exposure is the edge. When the pure-play space names correct on profit-taking or sentiment, the electronics names tend to hold better because their revenues are anchored in multi-year government contracts with predictable delivery schedules. TTMI’s 504% one-year return and MRCY’s 131% demonstrate that the market has begun to price this exposure more explicitly, but both still trade at significant discounts to pure-play space multiples despite having more durable revenue streams. The right approach is to treat this bucket as the quality anchor of a space allocation, a position you can hold through volatility without the same white-knuckle drawdown risk as the high-beta names. Size these larger, trade them less, and let the compounding defense contract cycle do the work.

Accompanying this report are two additional resources available to all subscribers: our 20-page chart book covering the full space stock universe with technical setups and relative strength analysis, and our 19-page consolidated research report — After Liftoff: The SpaceX IPO Has Landed — Now the Real Ecosystem Trade Begins — which documents our coverage of the space economy over the past two to three months. Together, they provide the complete analytical framework behind the positions and entry levels discussed above.